Tax benefits, government help and easy access to regional markets led Joe Seunghyun Cho to choose Singapore as the headquarters for his six financial technology companies, rather than base them in the rival hub of Hong Kong or his native South Korea.

“We are quite impressed by government agencies here,” said Cho, whose Marvelstone Group is developing a mobile payments platform and invests in other fintech firms. Singapore authorities introduced him to tax advantages and connected his firm to potent

Many fintech companies are making similar choices, adding a new dimension to the decades-old tussle between Singapore and Hong Kong for the position as Asia’s premier financial center. With banks’ profits under pressure from stricter global regulations and rising compliance costs, it’s a battle either city can ill afford to lose.

Interviews with fintech entrepreneurs and business consultants show that while Hong Kong is making strides to catch up, Singapore has the lead — in part because its government was quicker in recognizing the industry’s potential. In a February studycommissioned by the U.K. government, Ernst & Young LLP ranked the Southeast Asian city fourth among global fintech hubs, while Hong Kong came seventh. Singapore was the “preferred gateway” into Asia, the report said, highlighting the city’s “increasingly progressive regulatory regime.”

Growth Incentive

“Financial services is an important contributor to economic growth and jobs in these cities,” said Mohit Mehrotra, Deloitte LLP’s strategy consulting leader for Southeast Asia. “The industry is under lot of pressure to maintain its margin and growth. The key is to build up players that can supply innovative technology solutions to the financial services industry and support the growth of the ecosystem.”

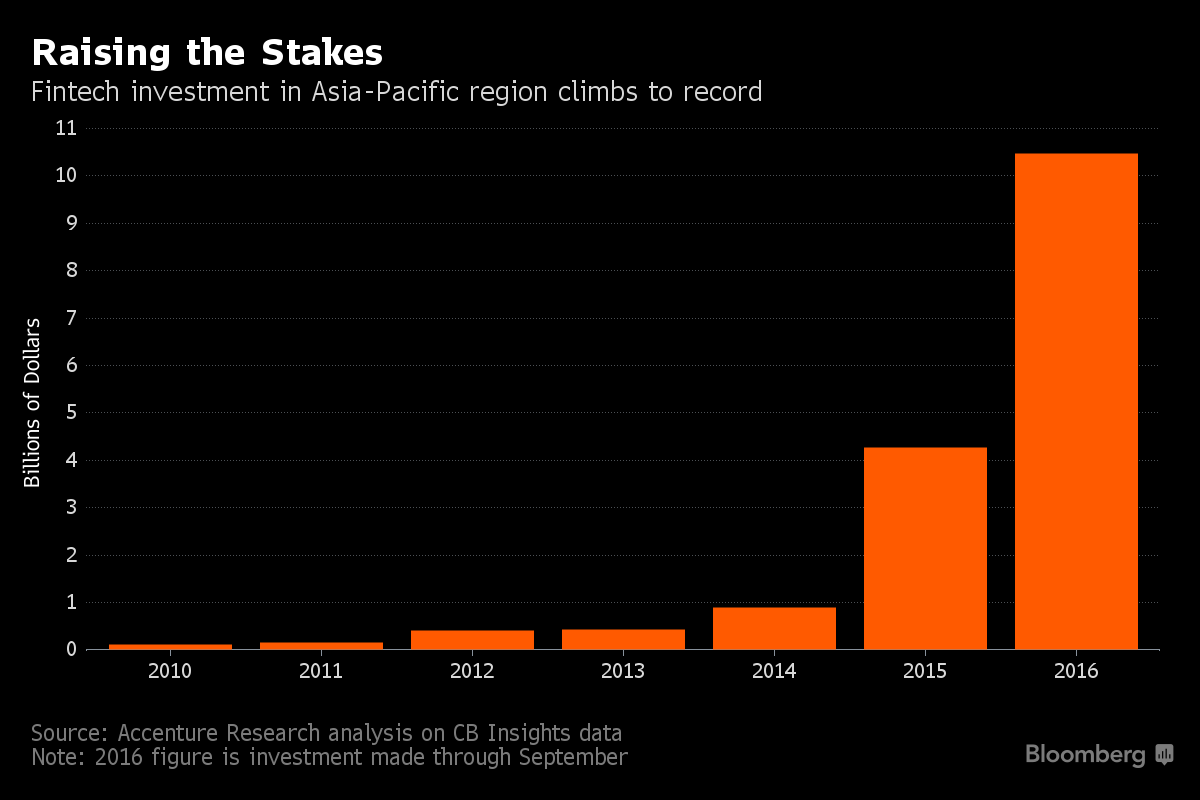

Companies and investors poured $10.5 billion into fintech in the Asia-Pacific region this year through September, about $2 billion more than in the Europe and the U.S. combined, according to an analysis by Accenture Plc based on CB Insights data. The bulk of that money went to mainland China.

The gap between Hong Kong and Singapore was on display last month when they hosted their own inaugural fintech conferences within a week of each other. The Singapore Fintech Festival drew more than 11,000 attendees and featured blockchain cheerleader Blythe Masters, ex-Standard Chartered Plc Chief Executive Officer Peter Sands and former Deutsche Bank AG head Anshu Jain as speakers. Hong Kong’s event the previous week drew less than a quarter of that number of participants.

“Singapore is extremely well positioned to back a hub of fintech activities that represents an avenue into the broader Asia markets,” Masters, who once ran JPMorgan & Chase Co.’s commodities business, said in an interview on the sidelines of the city’s conference.

Career Paths

For South African-born Shailesh Naik, picking Singapore over Hong Kong as the base for his mobile-payments technology company MatchMove Pay Pte came down to the supply of highly-skilled professionals, access to regional markets and the regulatory environment.

The Singapore government’s focus on startups and fintech provides “gravity and momentum for career paths,” he said. What’s more, it’s “easier to navigate in Singapore and nearby countries due to the use of English in business. This is a big point compared to Hong Kong.”

Since starting in 2009, MatchMove has expanded into India, Vietnam, Indonesia, Thailand and the Philippines, and now has 160 employees. Credit Saison Co., Japan’s third-largest consumer finance company by value, bought a stake in the firm in January 2015.

For Hong Kong, its traditional role as the financial gateway to mainland China has proved a mixed blessing. That’s because China, the home to Ant Financial, Lufax and other homegrown giants, already has a booming fintech industry. Almost 90 percent of fintech investment in Asia-Pacific this year bypassed both Hong Kong and Singapore and went directly into China, according to the Accenture study.

Fundraising Center

Undeterred, Hong Kong is moving to catch up. The Hong Kong Monetary Authority unveiled a Fintech Innovation Hub in September that seeks to bring banks, startups and central bank representatives together to develop and trial fintech ideas. The HKMA also set up a “sandbox” that allows companies to test their innovations in a loosely regulated environment before releasing them publicly — three months after Singapore proposed such a structure.

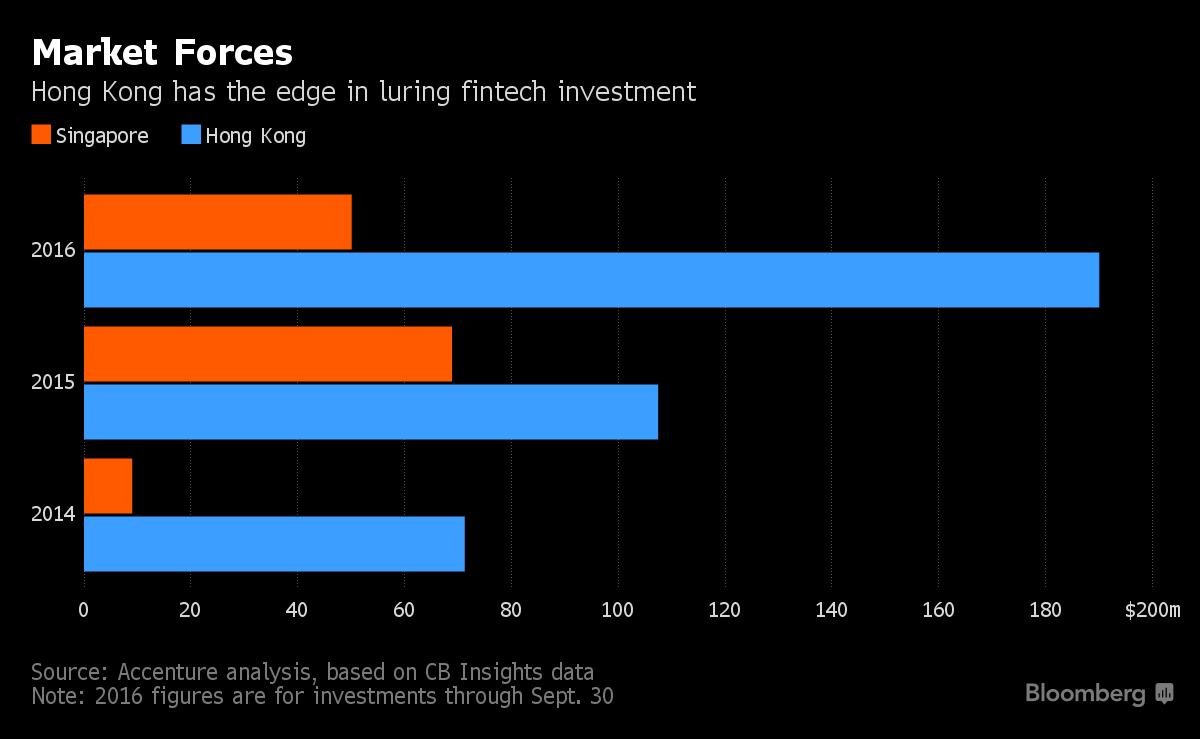

Hong Kong’s history as a mammoth fundraising center could allow the government to take a more hands-off approach than Singapore in bankrolling startups. The $369 million of investment into fintech in the city from the end of 2013 through Sept. 30 was almost triple Singapore’s haul, according to Accenture’s figures.

“Hong Kong is a highly open market with strong legislation but little governmental intervention,” Albert Wong, CEO of the Hong Kong Science and Technology Parks Corp., which operates research facilities for the government, said in an e-mailed reply to questions. “Therefore the development of fintech will be mainly, just as other market development in this city, be driven by market force.”

Still, Wong said startups in Hong Kong need better support in terms of seed capital and early-stage funding. What’s more, the city needs to take steps to improve its talent pool in technology and engineering, he said. The Ernst & Young study ranked Hong Kong higher than Singapore for availability of capital, but put the Southeast Asian city ahead in terms of talent and government policy.

‘Standing Start’

Strong backing from the Singapore government was a key factor for entrepreneurs like Marvelstone’s Cho and MatchMove’s Naik.

Cho said the Monetary Authority of Singapore helped introduce him to government agencies and other fintech firms, some of which became tenants at an office space his firm operates for startups in the central business district. The space, known as Lattice80, also houses the Singapore office of R3, the consortium of global financial firms that’s developing blockchain applications, as well as MatchMove.

The MAS has “been very clever in its approach in trying to define Singapore as a kind of innovation hub,” said James Lloyd, Ernst & Young’s Asia Pacific fintech leader. “Is Hong Kong starting behind Singapore in terms of figuring out what fintech is all about? Yes absolutely. But even in the last 12 months, Hong Kong has gone from a standing start to moving at least quicker than most people would have expected.”